Sensex Recovers 700 Points From Lows — But Can the Afternoon Hold the Gains?

- 4 hours ago

- 6 min read

Based on market data as of 13:06 IST on 04 June 2026.

At a glance

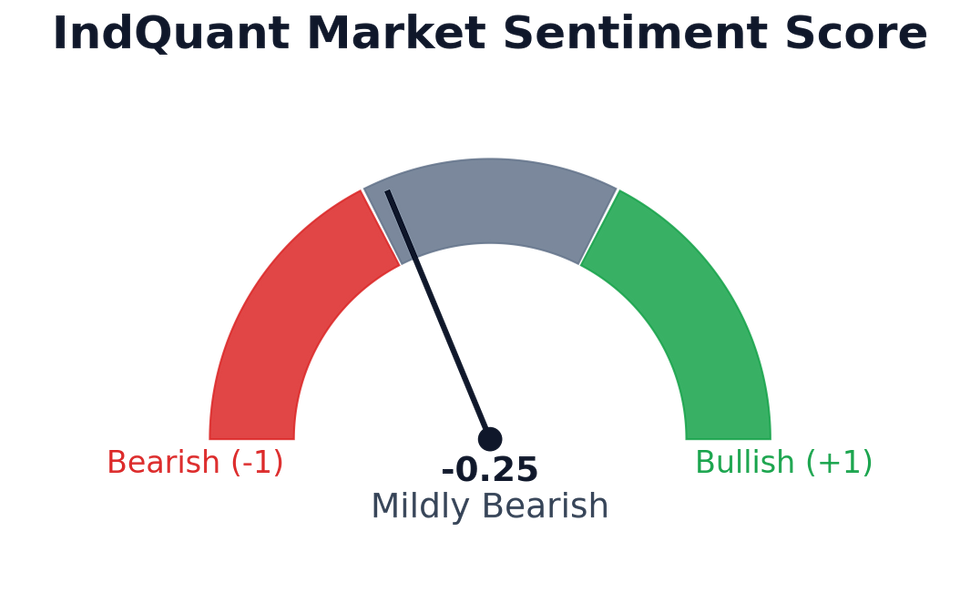

Sensex fell 300+ points at the open before recovering sharply; the overall sentiment score sits at -0.25, signalling a mildly bearish day that has partially stabilised by midday.

FII (Foreign Institutional Investor) selling, a rupee near record lows of ₹95–96 per US dollar, and the ongoing RBI (Reserve Bank of India) MPC (Monetary Policy Committee) rate decision are the three biggest overhangs heading into the afternoon.

Pharma is the lone bright sector; IT, Banking, and Auto are all in the red, though DIIs (Domestic Institutional Investors) are providing a floor around the 23,250 Nifty zone.

The setup

Midday on June 4, 2026, and Indian markets are at a delicate equilibrium. The morning selloff — triggered by FII outflows, West Asia tensions, and a weak rupee — has been partially absorbed, with Nifty clawing back from the 23,150 zone. But "recovery" is doing a lot of heavy lifting here. The broader picture remains cautious: 62% of Nifty 50 companies have seen earnings downgrades, the RBI MPC is still in session, and the afternoon could easily tilt either way depending on what the central bank signals and how global risk appetite evolves in the next two and a half hours.

Top 5 sentiment drivers

Risk factors. A rare convergence of headwinds is weighing on sentiment — West Asia conflict keeping Brent crude at USD 96.64, the rupee flirting with record lows near ₹95–96 per dollar, RBI MPC uncertainty with the repo rate (the rate at which RBI lends to banks) sitting at 5.25%, a SEBI (Securities and Exchange Board of India) fraud action against Rajesh Exports for alleged revenue inflation of ₹15.15 lakh crore (₹15,150,000 crore), and the Dallas Fed signalling possible further US rate tightening — all arriving simultaneously; the combined score is strongly bearish at -0.45.

Geopolitical risk premium. West Asia tensions remain the dominant geopolitical force, keeping Brent crude elevated and embedding a risk premium in gold, which is trading near ₹1.6 lakh (₹1,60,000) per 10 grams; the score is strongly bearish at -0.45, though US-Iran negotiations have contributed a modest 0.7% crude pullback that is providing some relief at the margin.

FII/DII flow sentiment. Persistent FII selling drove the Sensex down 300+ points at the open, with outflows partly linked to global firms repatriating profits from Indian IPO listings; the score is bearish at -0.40, but DII buying has stepped in firmly around the 23,250–23,150 Nifty support zone, preventing a deeper breakdown and creating the tug-of-war that the ICICI Prudential AMC CIO has described as a "boring phase" for markets.

Earnings momentum and corporate health. JM Financial's warning that FY27 (financial year ending March 2027) earnings growth could disappoint is finding confirmation in the data — 31 of the 50 Nifty 50 companies, or 62% of the index, saw EPS (Earnings Per Share) downgrades in May 2026 alone; the score is moderately bearish at -0.35, and with the sugar sector posting weak Q4 FY26 results and IT names under pressure, the earnings narrative is broadly negative heading into the second half of the session.

IT sector sentiment. TCS, Wipro, and Infosys are all declining, with Infosys among the top index losers as Nifty trades below 23,400; the score is moderately bearish at -0.35, and Broadcom's mixed results — 48% AI (Artificial Intelligence) revenue growth paired with disappointing forward guidance — have added fresh uncertainty about whether Indian IT firms can monetise the AI wave fast enough to offset slowing traditional business.

Sectors in focus

Banking. Mildly bearish at -0.30 — Bank Nifty fell to an intraday low of 53,829 before recovering to around 54,333, but HDFC Bank, Canara Bank, and PNB remain in the red even as SBI and IDFC First Bank lead the partial rebound; the RBI MPC's expected repo rate hold at 5.25% limits near-term re-rating potential for the sector.

IT. Moderately bearish at -0.35 — AI disruption fears are structural, not just a one-day story; Infosys is among the top Nifty losers today, and Broadcom's guidance miss overnight has reinforced the view that global tech spending remains uneven, making a meaningful IT rally unlikely before the closing bell.

Auto & Manufacturing. Mildly bearish at -0.15 — elevated crude at USD 96.64 squeezes input costs and dampens consumer sentiment for vehicle purchases; BHEL has been downgraded to Neutral by UBS with a target of ₹460, though Tenneco Clean Air is a bright spot, up 4% on a strong order book with JM Financial projecting 19% upside.

Pharma. The lone outperformer today, mildly bullish at +0.20 — defensive rotation into pharma is absorbing some of the FII selling pressure, Aurobindo Pharma is on watch for positive developments, and the absence of any fresh USFDA (US Food and Drug Administration) negative actions is allowing the sector to hold its gains as markets stabilise at midday.

Global and macro backdrop

Asian markets fell in early trade following a Wall Street retreat, with Brent crude slipping USD 1.17 to USD 96.64 on progress in US-Iran talks — a partial positive for India's import bill. However, the Dallas Fed President's comments suggesting further US policy tightening have dampened global risk appetite and are a headwind for FII flows into emerging markets like India. The rupee is trading near ₹95–96 per dollar, close to record lows, driven by FII outflows and profit repatriation by foreign firms that listed Indian subsidiaries. Gold near ₹1.6 lakh per 10 grams reflects safe-haven demand. The Cabinet is reportedly considering measures to attract foreign investors to Indian government bonds, which could provide medium-term rupee support but is unlikely to move markets today. China and Europe are low-signal for now, with China's regulatory stance marginally positive at +0.05 and Europe neutral at 0.00.

Risks to watch

RBI MPC outcome: Any surprise in tone — even if the repo rate holds at 5.25% — could swing Nifty sharply in either direction in the final 90 minutes of trade.

Crude oil reversal: If US-Iran talks stall or West Asia tensions escalate before 3:30 PM IST, crude could spike back above USD 97–98, reversing the afternoon calm.

Rupee slide: A further weakening past ₹96 per dollar could trigger fresh FII selling and pressure rate-sensitive sectors like banking and auto.

Volatility spike: India VIX (Volatility Index — a measure of expected market swings) is likely elevated; the Sensex has already swung 700+ points intraday, and any negative headline in the next two hours could amplify moves.

What this means for the rest of today's session

The market has done the hard work of recovering from its morning lows, but the afternoon is not a free pass. The RBI MPC statement is the single biggest variable — a hawkish hold or any commentary flagging rupee or inflation concerns could undo the midday recovery quickly. If the MPC tone is neutral and crude stays below USD 97, DII support around 23,250 Nifty should hold and the session could close with modest losses rather than a sharp selloff. Pharma and select energy names look like the steadier ground for the remainder of the day, while IT and banking remain vulnerable to any fresh negative headline before the 3:30 PM closing bell.

How to read this

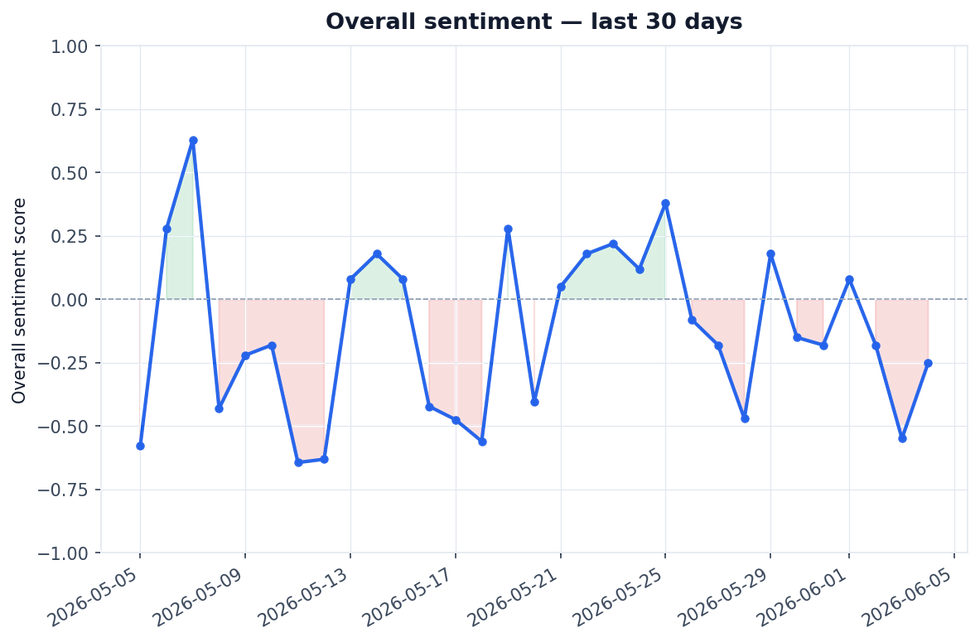

What this sentiment is measuring. We score 16 distinct dimensions of market sentiment, covering broad market direction, key sectors (banking, IT, auto and manufacturing, pharma), global cues, FII / DII flows, currency and commodities, regulatory stance across India and major foreign jurisdictions, and risk indicators. Each dimension is given a score from −1 (strongly bearish) to +1 (strongly bullish), paired with a 0 to 1 confidence weight that reflects how much supporting evidence the model found. The overall score shown in the dial is a confidence-weighted blend of all dimensions on the same −1 to +1 scale.

What data is used. The analysis draws on Indian and global financial news, regulatory and policy feeds from India as well as major foreign jurisdictions, and market news from global exchanges. News items are filtered for freshness and relevance before being scored, so the picture reflects what the market is reading and reacting to right now.

Limitations. This article is not investment advice and not a recommendation to buy, sell, or hold any security. The output is best treated as a structured attribute set — useful as one input among many when building your own prediction models or sense-checking your own view, not as a forecast on its own.

Comments