Nifty Holds 24,200 Early On, But IT Drag Keeps Gains Fragile

- 6 hours ago

- 6 min read

Based on market data as of 10:05 IST on 17 April 2026.

At a glance

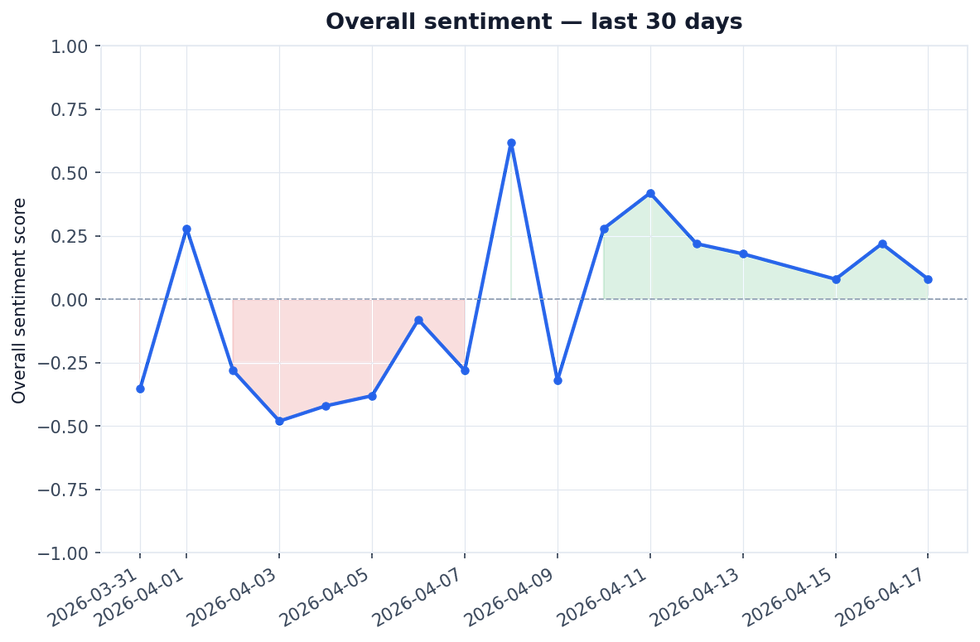

Nifty is trading above 24,200 and Sensex is up roughly 150–161 points about 45 minutes into the session, with overall sentiment mildly bullish at +0.08.

Wipro shares have fallen ~4% after a weak Q4 result, making IT the biggest drag on the index right now.

Crude oil sliding to $98.17 on Iran-US peace hopes is the key tailwind, supporting the rupee and India's import bill outlook.

The setup

Forty-five minutes into Friday's session, Indian markets are holding a cautious positive bias — but the word "cautious" is doing a lot of work here. The Nifty is clinging to the 24,200 level and the Sensex is up around 150–161 points, yet the gains feel earned rather than effortless. Two forces are pulling in opposite directions: a meaningful drop in crude oil prices driven by Middle East peace diplomacy is giving bulls something to work with, while a disappointing quarterly result from Wipro is reminding the market that earnings season can bite. The session's overall sentiment score sits at a barely-positive +0.08 — essentially a tug-of-war, with the outcome still open.

Top 5 sentiment drivers

IT sector sentiment. Wipro's Q4 FY26 (the quarter ending March 2026) net profit fell 1.89% year-on-year (YoY) to ₹3,501.8 crore (approximately ₹35 billion), and the stock has dropped ~4% in early trade; weak revenue guidance is now sparking sector-wide anxiety, with Goldman Sachs and three other brokerages flagging concerns — making IT the single biggest drag on Nifty right now, with a moderately bearish score of -0.45.

Currency and commodity impact. Brent crude — the global oil benchmark — fell 1.23% to $98.17 per barrel on Iran-US peace talks and an Israel-Lebanon ceasefire, easing pressure on India's Current Account Deficit (CAD, the gap between what India earns and spends in foreign exchange); this is mildly bullish at +0.30, as softer crude also supports the Indian Rupee (INR) and keeps retail inflation expectations in check.

Auto and manufacturing outlook. Bosch Chairman Stefan Hartung publicly backed India's growth story, forecasting high single-digit revenue growth for the company's India operations in 2026 despite global headwinds; separately, the government's formation of an AI Governance and Economic Group (AIGEG) signals continued policy support for manufacturing — together pushing this driver to a mildly bullish +0.30, with defence and metals stocks also holding up well in early trade.

Geopolitical risk premium. The Middle East ceasefire is fragile, and Asian markets are slipping on that uncertainty; Europe is assembling a 30-nation coalition to protect the Strait of Hormuz — the critical shipping lane through which a large share of global oil flows — without the US, Israel, or Iran, which signals the risk is far from resolved; this keeps the geopolitical risk score at a mildly bearish -0.20.

Risk factors. Beyond geopolitics, a potential strike at an Australian LNG (Liquefied Natural Gas) plant threatens global energy supply, LPG prices in India have already been revised once due to West Asia disruptions, and the Enforcement Directorate's (ED) custody of former Reliance Group executives adds a regulatory-risk undercurrent to the session — collectively a mildly bearish -0.20 that investors should keep on their radar.

Sectors in focus

Banking. Mildly bullish at +0.20 — HDFC AMC and HDFC Life are both reporting Q4 results today, and Jio Financial Services is in focus ahead of its own results and a potential dividend announcement; with no major negative triggers for Bank Nifty and the broader market holding up, banking stocks are finding quiet support, though institutional flow direction remains unclear.

IT. Moderately bearish at -0.45 and the clear laggard of the morning — Wipro's profit decline and soft guidance have put the entire sector on the back foot, with Goldman Sachs and peers cautious; a Supreme Court hearing in the TCS Nashik employee case adds a legal overhang, making IT the one sector where early-session weakness is most visible.

Auto & Manufacturing. Mildly bullish at +0.30 — Bosch's India confidence and the government's AIGEG formation are positive signals for the manufacturing ecosystem; defence stocks are holding their ground even as broader indices chop around, and metals are showing resilience, making this pocket one of the relative bright spots in today's early trade.

Pharma. Barely positive at +0.10 and low-conviction — China's National Development and Reform Commission (NDRC) announced improvements to its drug price formation mechanism, which could affect Indian pharma companies' export competitiveness in that market; on the positive side, Middle East peace hopes reduce supply-chain disruption risk for Active Pharmaceutical Ingredients (APIs), and the broader market's mild recovery is providing a floor.

Global and macro backdrop

The global backdrop is mixed but not alarming. Asian markets are dipping on Middle East uncertainty, yet the S&P 500's recent recovery to all-time highs after a 9% drawdown suggests global risk appetite has not collapsed. Brent crude at $98.17 is the most consequential global number for India today — every dollar drop in oil meaningfully improves India's CAD and keeps the Reserve Bank of India's (RBI) inflation management task easier.

On flows, FII (Foreign Institutional Investor) and DII (Domestic Institutional Investor) direction is not yet clear for today's session, with confidence on flow data low at this early hour. The INR is expected to benefit from softer crude and peace-talk optimism, which would be a mild positive for import-heavy sectors. On the regulatory front, the government's AIGEG formation is a quiet but forward-looking positive for India's technology and manufacturing policy environment. The Securities and Exchange Board of India (SEBI) and RBI frameworks are stable, with no new adverse actions detected this morning.

Risks to watch

Wipro contagion: If weak guidance from Wipro triggers downgrades across the IT sector, selling pressure could broaden beyond just one stock and weigh more heavily on Nifty.

Hormuz fragility: The 30-nation European coalition forming around the Strait of Hormuz — without the US, Israel, or Iran — signals the energy corridor remains at risk; any escalation could reverse crude's decline sharply.

Australia LNG strike: A potential industrial strike at an Australian LNG plant could tighten global gas supply and push energy prices higher, adding to India's import cost pressures.

Intraday choppiness: Nifty has already oscillated between 24,149 and 24,200+ in the first 45 minutes, suggesting VIX (the Volatility Index, a measure of expected market swings) conditions remain elevated; profit booking could intensify if key levels break.

What this means for the rest of today's session

The rest of today's session is likely to remain range-bound and stock-specific. The broad index has a mild positive bias thanks to crude's decline and peace-talk optimism, but IT's underperformance is a real ceiling on how far the rally can extend. Investors will be watching HDFC AMC, HDFC Life, and Jio Financial Services results as they land, since banking and financial stocks could provide the next directional cue. If crude holds below $100 and no fresh geopolitical shock emerges before the closing bell, the Nifty has a reasonable chance of finishing the day modestly in the green — but the margin for error is thin heading into the weekend.

How to read this

What this sentiment is measuring. We score 16 distinct dimensions of market sentiment, covering broad market direction, key sectors (banking, IT, auto and manufacturing, pharma), global cues, FII / DII flows, currency and commodities, regulatory stance across India and major foreign jurisdictions, and risk indicators. Each dimension is given a score from −1 (strongly bearish) to +1 (strongly bullish), paired with a 0 to 1 confidence weight that reflects how much supporting evidence the model found. The overall score shown in the dial is a confidence-weighted blend of all dimensions on the same −1 to +1 scale.

What data is used. The analysis draws on Indian and global financial news, regulatory and policy feeds from India as well as major foreign jurisdictions, and market news from global exchanges. News items are filtered for freshness and relevance before being scored, so the picture reflects what the market is reading and reacting to right now.

Limitations. This article is not investment advice and not a recommendation to buy, sell, or hold any security. The output is best treated as a structured attribute set — useful as one input among many when building your own prediction models or sense-checking your own view, not as a forecast on its own.

Comments